Long-Term Expected Return of Collectibles

Executive Summary Stores of value represent an alternative asset class compared to stocks, bonds, and real estate. Examples include gold and silver bullion, many cryptocurrencies and NFTs, collectibles, and art. Stores of value do not generate income, and while most have some utility, their primary financial use is to hold value over the long-term in line with inflation and global wealth. Gold bullion and gold jewelry make up most the store of value market cap at $12 trillion. The global art market is valued at over $1 trillion. The crypto market recently peaked at $2.9 trillion. The global collectibles market is much smaller, in the $500 billion range. By comparison, the global market cap of bonds, stocks and real estate are many multiples of world GDP, on the order of $500 trillion. The current investment environment is favorable to stores of value as a partial replacement for bonds as part of a diversified portfolio. Store of value assets provide inflation protection, portfolio...

read more

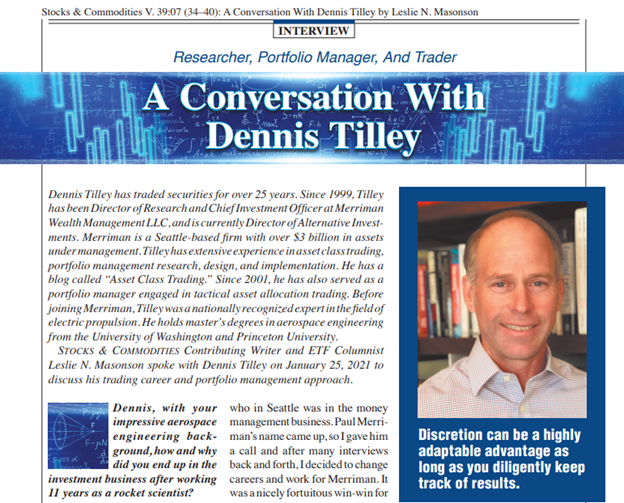

Interview with Dennis Tilley

I was recently interviewed by Technical Analysis of Stocks and Commodities, and my interview was published in the July 2021 issue.

read more

Two Unappreciated Compelling Reasons to Own Gold in the 2020s

Executive Summary There are many smart investors who’ve taken a shining to gold in recent years. Their reasons are many, including negative real interest rates around the world, central bank buying, and rapidly rising production costs. In addition, gold can provide insurance for all sorts of nasty financial outcomes that appear quite possible due to excessively high debt-to-GDP levels and high wealth inequality. Such outcomes and worries include the rise of populism, money printing, trade wars, competitive devaluations, unconventional monetary policies, an unexpected rise of inflation and the vulnerability of the U.S. dollar to a significant decline. Even a run-of-the-mill recession may trigger significant pain and uncertainty for the markets. In this post, I discuss two unappreciated and compelling reasons to own gold that go beyond what is mentioned above. The first is that gold is significantly under-owned among U.S. investors. Many investors think they’re covered by owning a few...

read more

Asset-Class Value Traps and Catalysts to Avoid Them

Executive Summary In the last of our asset-class valuation series, I discuss costly value traps that can derail even the best-reasoned asset-class value themes. A lot can go wrong when you bet on value. In particular, an asset class that appears to be an excellent value can stay that way for years. All investors face this problem and most professional investors who manage billions of dollars have only one option, which is to leg into these investments over time. Asset class traders have the benefit of being small enough to wait for a catalyst before trading a compelling value opportunity. In this blog post, I review various catalysts I use to get the timing right and avoid the value traps. Introduction Most traders and investors know to be aware of value traps when investing in cheap assets. Value investors comment that risk of permanent loss is the true risk associated with investing, and a worst-case scenario is losing 100% of capital. Although asset classes rarely lose 100% of...

read more

Compelling Value

Executive Summary Asset classes trading significantly below intrinsic value occur infrequently, perhaps once every 10-20 years per asset class. We need to accept that asset pricing (for long hold periods) is rational and correct most the time, and that cheap asset classes are usually cheap for a reason. I discuss methods I use to determine when an asset class is irrationally mispriced well below long-term intrinsic value. I’m trying to distinguish a once-a-decade compelling valuation versus run-of-the-mill everyday value opportunities. Compelling values set up lucrative multi-year trades to the long side. While there’s no formula for identifying these opportunities, I present three steps I take in the search. First, I find prices that appear to be an extreme outlier with respect to history, logic and other asset class valuations. Second, I identify the behavioral effect causing the asset class to be mispriced compared to long-term intrinsic value. Finally, I ask myself a few...

read more

Shiller CAPE – A Deceptively Dangerous Tool

Executive Summary In this post, I examine the popular stock market valuation tool, the Shiller CAPE. The Shiller CAPE valuation approach, based on 150 years of data, appears to have an uncanny ability to predict future S&P 500 returns. Unfortunately, the benefits of using this tool for actual investment decisions appear to be limited. The Shiller CAPE, along with all asset class valuation measures, has the following significant weaknesses and issues. Selection bias has likely overstated the reliability of predicting future expected returns. Using CAPE to shift between equities and T-bills doesn’t enhance risk-adjusted returns. Using historical valuation data is susceptible to unpredictable long-term regime shifts that can devastate the effectiveness of such a tool. When the Shiller CAPE is low, risks are high, and many competing asset classes are also priced cheaply. When the CAPE is high, competing assets also have low expected returns. It appears the S&P 500 is efficiently...

read more

Value Investing for Asset Class Traders

Executive Summary This is the first of a multi-part series examining the use of valuation approaches to identify future outperforming asset classes. I discuss why value investing is an essential and useful tool for asset class traders. I briefly discuss the Warren Buffett approach as the purest form of discretionary value investing. I clarify the distinction between fair value (a concept I’ve used to discuss short-term trading edges) and intrinsic value used by value investors. I briefly review the vast academic literature on mechanically value-tilted portfolios. These portfolios are typically heavily weighted towards cheap and risky assets. These cheap securities are most often fairly priced to deliver long-term returns that are superior to a market cap weighted basket of similar securities. Finally, I introduce Asset Class Value Investing as: identifying moments in time when an asset class appears to be irrationally mispriced based on an assessment of long-term intrinsic value....

read more

Navigating Asset Bubbles for Profits

Large price runups, such as a gain of 100% over two years, are rare.1 In a previous blog post, I presented 10 attributes to distinguish asset class bubbles from large price runups that are justified by improving fundamentals. Those bubble attributes are: Heavy retail investor involvement New-era thinking Irrational valuations Five or more years of swiftly rising prices Parabolic rise in price Shorting is unattractive or impossible Social mania Product providers exploit excessive demand Leverage fuels more buying Bubbles are late-cycle phenomena As asset class traders, we are especially interested in bubbles as a potential huge source of alpha when they collapse. As it turns out, bubbles are a lot tougher to exploit than it might seem. In this blog post, we’ll delve into bubble characteristics in more detail, and then investigate the best ways to trade asset classes that are experiencing a bubble. We’ll examine bubble characteristics over the short term (plus and minus three years...

read more

Bubbles

If you’re in the investment biz long enough, you’ll inevitably find yourselves searching for profitable ideas when an asset class is experiencing a bubble. The term “bubble” is a heavily overused term in the financial media and among professional investors. Any large price increase over a short time period, such as a 50% gain over a year, prompts a few writers, analysts or professional investors to describe the runup as a bubble. These bearish folks are typically using the term loosely without a nuanced evaluation to determine if prices have simply reflected new highly positive information. Additionally, how many times have we heard “bubble” used for assets that have experienced long-term, secular bull markets, such as U.S. or Japanese government bonds, when current prices are not experiencing anything like the bubble phenomenon? Then other folks use the term in a variety of ways to describe investor group think, such as “hedge funds are the next investment bubble,” or “there’s...

read more

Long-Term Relative Strength Line Trend Changes

Often in trading we become totally engrossed in searching for short-term opportunities with a hyper-focus on news flow and daily price movements. Occasionally it’s good to drastically alter time frames, especially if your creativity has dried up on short-term ideas. One way to search for new trades is to scan asset classes that have performed the worst over the previous decade. This is especially interesting when there’s been a large divergence of performance in asset class returns over the previous 5 to 10 years. Table 1 shows a ranking of the worst-performing ETFs by 10-year annualized returns as of October 31, 2017. When tabulating this ranking, I excluded the ProShares daily leveraging funds and commodity exchange traded notes. For comparison, the S&P 500 returned 7.51% per year during this time frame. This list contains many ETFs in the energy space, with a few niche asset classes (clean energy, gold miners, steel and nuclear), country funds (Russia, Italy and Brazil) and...

read more